Introduction

This white paper complements the openfunds white paper ‘Countries of Registration’. While the document ‘Countries of Registration’ focuses on the openfunds concept for regulatory approval and marketing status of a fund in individual jurisdictions, the present whitepaper concentrates on the legal structure of a fund in its home domicile and the resulting implications for investor eligibility.

Both topics are closely related, but have been separated into two documents to keep the respective concepts clearly distinguishable.

This white paper addresses the following openfunds fields:

OFST160169 Home Country Legal Structure ID

OFST160170 Home Country Legal Structure of Fund

OFST6030XX Country Legal Registration

OFST6031XX Country Marketing Distribution

OFST6060XX Investor-specific Exclusion

- Quick link to reference table here.

Scope of this White Paper

This document focuses on the classification of fund structures in their home jurisdiction. It does not attempt to provide a comprehensive legal description of each structure. The definitions provided are intended to support consistent data reporting within the openfunds framework.

Interpretation Principle

When mapping a fund to a Home Country Legal Structure, the classification assigned by the competent regulator should take precedence over informal market terminology or tax classifications.

Home Country Legal Structure (OFST160170)

The Home Country Legal Structure of a fund describes the regulatory classification assigned to a collective investment scheme by the competent authority (NCA) in the fund’s home jurisdiction.

It is specifically important to distinguish between the following classification concepts, as both are touching legal aspects and are often mixed up:

- the legal form of a fund (OFST160100 “Legal Form”), which describes the legal constitution of the vehicle (e.g. contractual fund, corporate fund, limited partnership), and

- the regulatory classification assigned by the national competent authority (e.g. LTAF (UK), L-QIF (Switzerland), QIAIF (Ireland), RAIF (Luxembourg), etc.).

Depending on the regulatory classification, certain investor categories may be explicitly permitted or excluded.

Implied Investor Restrictions

Investor restrictions refer to regulatory or contractual limitations defining which categories of investors are permitted or prohibited from investing in a fund. Although the exact terminology differs across jurisdictions, the concept generally covers restrictions arising from regulatory structure, marketing approval, or explicit exclusions defined in the fund documentation.

- Regulatory classification in the home jurisdiction:

The domestic legal structure of a fund may inherently restrict the eligible investor base. For example, a Swiss Limited Qualified Investor Fund (L-QIF) may only be offered to qualified investors.

This information is captured by OFST160170 “Home Country Legal Structure of Fund”. - Registration and marketing approval in foreign jurisdictions:

When a fund is distributed outside its home jurisdiction, local regulatory approval may restrict distribution to certain investor categories.

This information is captured by OFST6030XX “Country Legal Registration” and OFST6031XX “Country Marketing Distribution”. More details are described in the openfunds white paper ‘Countries of Registration’. - Explicit investor exclusions defined in the prospectus:

Fund documentation may explicitly prohibit investment by certain categories of investors (for example, “US persons”).

This information is captured by OFST6060XX “Investor-specific Exclusion”.

Differentiation to MiFID Target Market

It is important to distinguish between MiFID target market information and investor restrictions. The MiFID target market describes the categories of investors for whom a financial product is considered appropriate (a positive definition).

Investor restrictions or exclusions, by contrast, describe categories of investors who are not permitted to invest in the product (a negative definition).

Definition of investor types

With the current concept of OFST160170 “Home Country Legal Structure of Fund”, openfunds provides indicative information regarding the categories of investors that may be permitted or excluded for certain fund structures.

However, the terminology and legal definitions of investor categories (such as retail investors, professional investors, qualified investors, accredited investors, or institutional investors) vary significantly across jurisdictions and regulatory frameworks.

For this reason, openfunds intentionally does not attempt to provide a harmonised legal definition of investor types across jurisdictions, nor does it aim to replicate the detailed regulatory definitions applied by national authorities.

Users of the openfunds data model are therefore expected to verify the applicable investor eligibility rules in the relevant jurisdictions and obtain legal advice where necessary. The information provided by openfunds is collected on a best-effort basis and serves as a technical data reference only; it does not constitute a legal assessment of investor eligibility.

Technical Representation of the Legal Structure by ID (OFST160169)

In addition to the descriptive field OFST160170 “Home Country Legal Structure of Fund”, openfunds provides a corresponding identifier field OFST160169 “Home Country Legal Structure ID”.

This identifier serves as a technical representation of the legal structure and is intended for use in automated data exchange. As the textual values of OFST160170 may be lengthy, language-dependent or contain special characters, the use of a standardised identifier facilitates consistency and interoperability between systems. The identifier itself does not carry intrinsic meaning and must always be interpreted using the corresponding reference table. Both sender and receiver are expected to maintain a mapping between the identifier and its associated description.

The format of the identifier follows a structured pattern of [ISO 3166-1 alpha-2 country code + “-“ + four-digit numeric code].

Example for an Irish legal structure: ‘IE-0002’ represents “Retail Investor AIF (RIAIF)”.

The identifier remains stable over time, including for historical or discontinued classifications, ensuring consistent reference across datasets.

Large variation by jurisdiction

The classification of investment funds varies significantly across jurisdictions. Some jurisdictions maintain a large number of regulatory structures (for example France with around 29 scheme types), while others operate with a comparatively small set of structures (for example Ireland with currently 3 schemes).

As a result, the level of granularity in the field OFST160170 “Home Country Legal Structure” per jurisdiction can differ substantially depending on the domicile of the fund. The field is designed to be setup at fund level, as the regulatory classification normally applies to the entire scheme rather than individual share classes.

Structural scheme vs. tax scheme

In certain jurisdictions, several classification layers exist simultaneously, which can make the regulatory landscape difficult to interpret if all dimensions are combined. These layers may include:

- the regulatory scheme type defined by the competent authority,

- the legal structure of the fund, and

- tax classifications or specialised regimes.

In order to maintain a consistent and manageable classification model, openfunds focuses primarily on the regulatory scheme classification defined by the national competent authority.

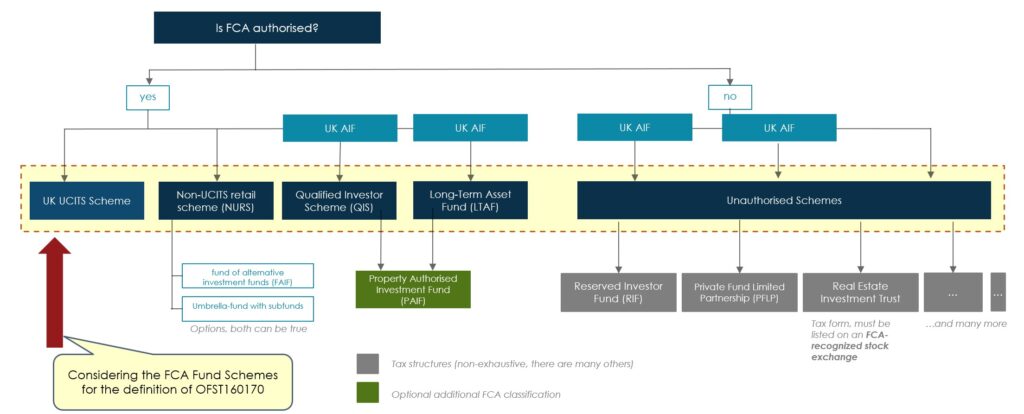

Example: UK

The United Kingdom provides a good example of such a multi-layered classification system. The UK Financial Conduct Authority (FCA) defines a set of authorised fund scheme types, including:

- UCITS Scheme

- Non-UCITS Retail Scheme (NURS)

- Qualified Investor Scheme (QIS)

- Long-Term Asset Fund (LTAF)

These classifications form the primary regulatory categorisation of authorised collective investment schemes in the UK and are therefore used by openfunds for the field OFST160170 “Home Country Legal Structure of Fund”.

Additional structures, such as Property Authorised Investment Funds (PAIF), Reserved Investor Funds (RIF), Private Fund Limited Partnerships (PFLP), or Real Estate Investment Trusts (REITs), represent tax regimes, legal vehicles, or unauthorised investment structures that may overlap with the regulatory classification but do not replace it.

Figure 1 illustrates how these different layers relate to each other (click here to enlarge the picture).

The diagram illustrates the hierarchy of UK fund classifications. The FCA distinguishes between authorised schemes (such as UCITS, NURS, QIS and LTAF) and unauthorised schemes. Additional structures such as RIF or PFLP represent tax regimes or legal vehicles that may coexist with the primary regulatory classification, whereas a PAIF can be set up in the form of a QIS or as an LTAF.

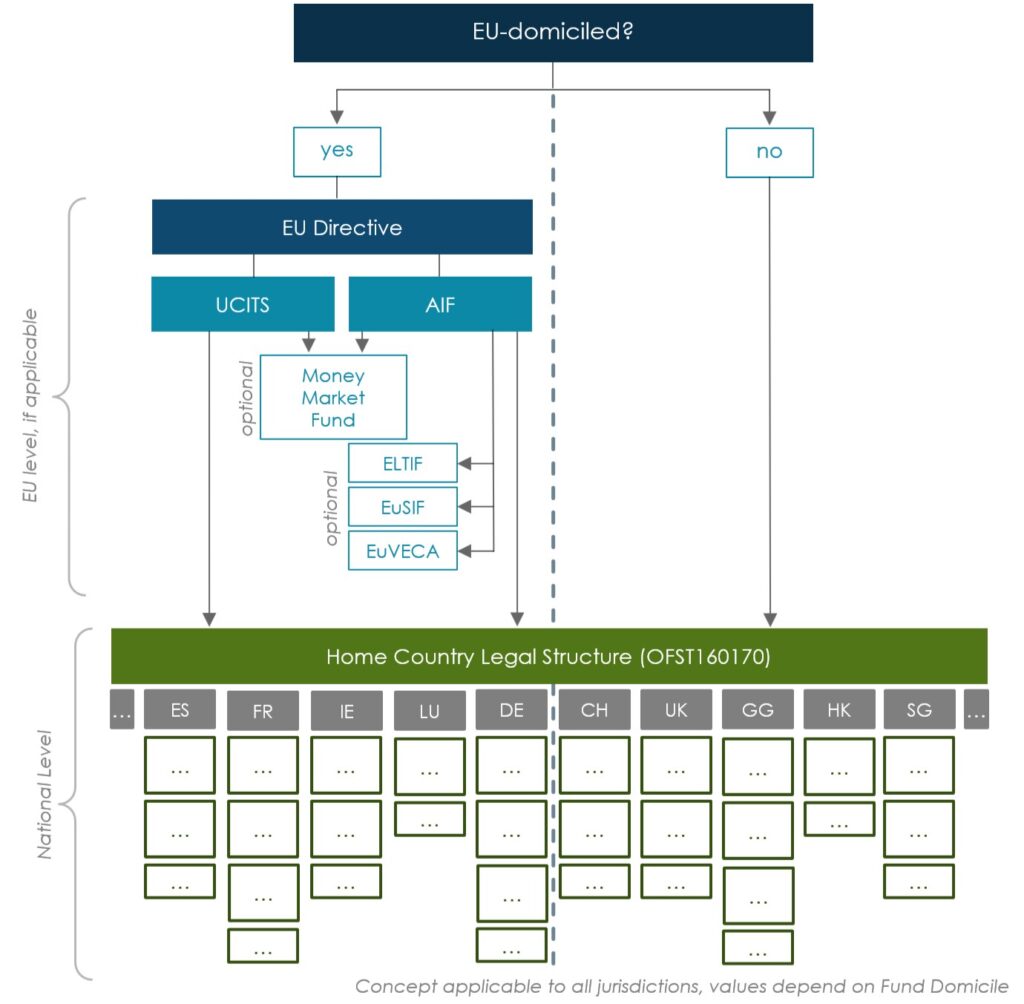

EU regulation vs. national schemes

There are several EU directives, regulations and frameworks in place which classify a fund on an EU- (supranational) level. The MiFID Directive and the AIFMD Directive have been adopted by the member states and have been transposed into local law. Several EU labels such as ‘Money Market Fund’, ‘ELTIF’ etc. are not mutually exclusive with national legal structures. For example, a fund may simultaneously qualify as a national RAIF in Luxembourg and as an ELTIF.

The corresponding information is captured in openfunds via dedicated fields such as:

- OFST160039 Is EU Directive Relevant

- OFST160040 Type of EU Directive

- OFST351295 Is Money Market Fund

- OFST351300 Money Market Type Of Fund

- OFST160042 Is ELTIF

- OFST160043 Is EuVECA

- OFST160044 Is EuSEF

Reference Table for National Legal Structures

Regulatory classifications evolve over time and new fund structures are introduced periodically. At the same time, legacy structures may remain relevant for historical data.

For this reason, openfunds maintains the list of valid values (IDs, names) in a dedicated reference table available here. Each value is represented by both a descriptive label (OFST160170) and a corresponding technical identifier (OFST160169). The identifier enables efficient data exchange, while the description provides human-readable context.

This table is maintained independently from the regular openfunds field releases.

Each version of the reference table identifies:

- newly introduced structures,

- modified definitions, and

- deprecated (retired) structures.

Document Information

| Title: | Home Country Legal Structures |

| Language: | English |

| Confidentiality: | Public |

| Authors: | openfunds (Birgit Partin) |

Revision History

| Version | Date | Status | Notice |

| 1.0 | 2026-03-19 | Final | First version. |

| 0.9 | 2026-03-09 | Draft | Initial version. |

Implementation

If you have any questions about openfunds or difficulties with implementation please contact us at businessoffice@openfunds.org.

Joining openfunds

If your firm has a need to reliably send or receive fund data, you are more than welcome to use the openfunds fields and definitions free-of-charge. Interested parties can contact the openfunds association by sending an email to: businessoffice@openfunds.org

openfunds.org

c/o Balmer-Etienne AG

Bederstrasse 66

CH-8002 Zurich

Email: businessoffice@openfunds.org

If you wish to read or download this white paper as PDF, please click here.