This white paper addresses the following openfunds fields:

OFST6030XX Country Legal Registration

OFST6031XX Country Marketing Distribution

Country Registration Information

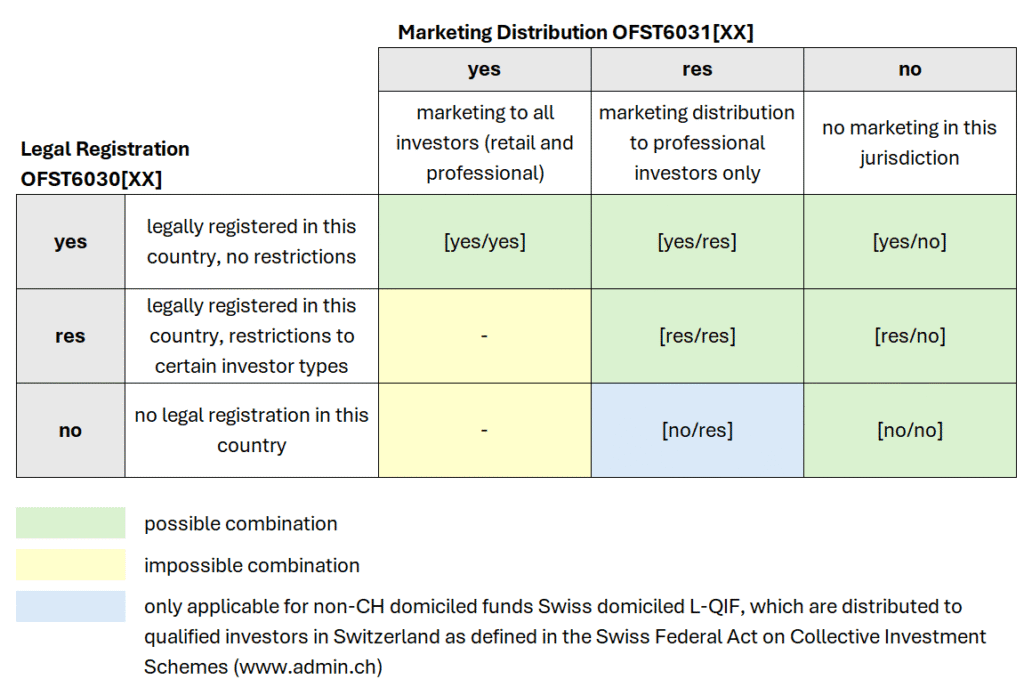

As the countries of legal registration and marketing distribution are essential not only for any marketing and sales activities, but also for suitability and dissemination of data, it is very important to understand the matrix of combinations and their impact on availability/visibility.

The values for both data points (OFST6030[XX] and OFST6031[XX]) are always required. Therefore, please ensure to populate information for each country by reflecting data in both data fields with the appropriate information.

Legal Registration (OFST6030[XX])

The ‘Legal Registration’ information per country reflects whether the ISIN is registered in this country from a legal perspective.

- ‘yes’ – this fund/share class is registered by the local financial authority for retail investors without restriction to a certain audience (i.e. institutional investors).

- ‘res’ – the approval of this fund/share class has been restricted by the local financial authority to a certain audience (i.e. institutional investors). ‘res’ also applies for funds passported in Europe to professional investors according to the AIFMD directive.

- ‘no’ – this fund/share class is not registered nor approved by the local financial authority of this country.

Marketing Distribution (OFST6031[XX])

‘Marketing Distribution’ is an additional filter regarding the availability to investors in a specific country. By restricting access to certain share classes to a limited audience only (‘res’) or no audience at all (‘no’), you can provide detailed instructions that support your marketing intentions per country. Please ensure to avoid ‘impossible combinations’ (see graphic above).

- ‘yes’ – this share class can be made available to all investors, including retail ones.

- ‘res’ – access to this share class should be restricted to a certain audience only (i.e. professional investors).

- ‘no’ – instruction to set visibility of this share class in the corresponding country to zero. If the fund/ share class is not registered in this country, this is the correct option to choose (exception of Switzerland see below).

Country specific approach

There are certain countries or fund types which have a specific rule set regarding the combinations of ‘Legal Registration’ and ‘Marketing Distribution’. Please find some details below, but keep in mind that this list does not provide any legal advice, as it is solely reflecting openfunds’ view.

If you require specific information regarding registration status of your fund range, please contact your legal department.

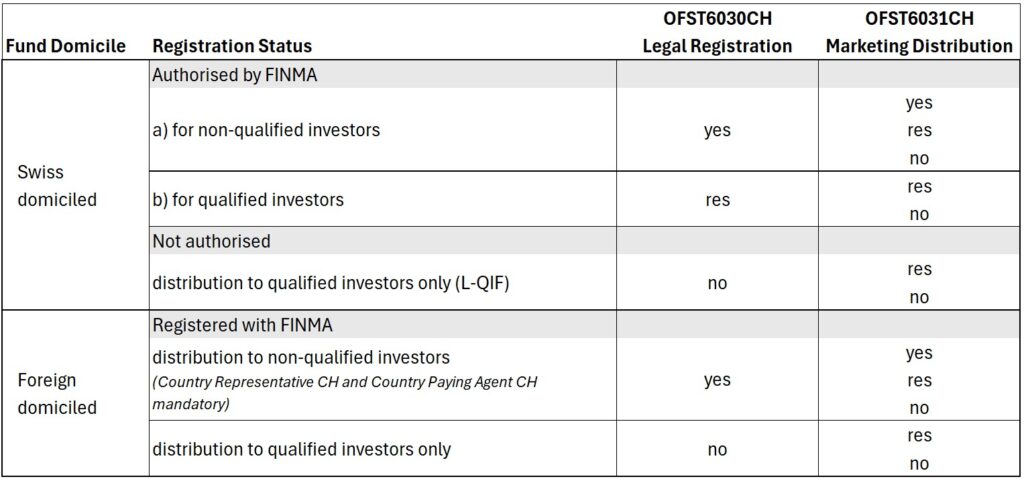

Switzerland

According to openfunds understanding, there are different legal approval types or marketing options to qualified investors for funds in Switzerland. Differentiation is made by the funds’ domicile being non-Swiss (‘foreign’) or Swiss:

Please note that for foreign funds registered/offered to non-qualified investors in Switzerland, the indication of following data is mandatory:

- Has Country Representative – Switzerland (OFST6100CH)

- Country Representative Name – Switzerland (OFST6102CH)

- Has Country Paying Agent – Switzerland (OFST6105CH)

- Country Paying Agent Name – Switzerland (OFST6107CH)

Please ensure to list the representative’s name in accordance to the official spelling of FINMA.

Furthermore, both foreign and domestic funds offered exclusively to qualified investors do not require approval by the Swiss regulator, Swiss Financial Market Supervisory Authority (FINMA).

For domestic funds, this framework is implemented through the Limited Qualified Investor Fund (L-QIF) regime.

Following the entry into force of the Financial Services Act (FinSA) on 1 January 2020, foreign funds offered exclusively to qualified investors (with the exception of high-net-worth individuals) are no longer required to appoint a Swiss Representative or Swiss Paying Agent. This represents a significant simplification compared to the previously applicable regulatory framework.

Further information on L-QIF is available on the FINMA website:

- https://www.finma.ch/en/authorisation/asset-management/swiss-collective-investment-schemes/ and

- https://www.finma.ch/en/news/2024/02/23240223-meldung-l-qif/

By combining the information on the fund’s domicile with the legal registration data (OFST6030CH) and the marketing distribution information (OFST6031CH), the fund’s registration status and the categories of permitted investors can be derived.

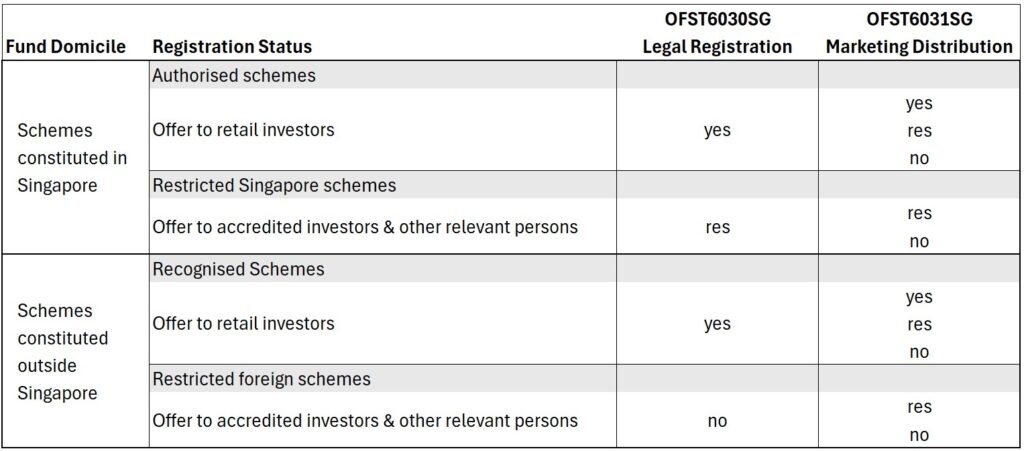

Singapore

According to the Monetary Authority of Singapore (MAS), there are different approval types in Singapore. Like Switzerland, there is a differentiation between Singapore constituted schemes and schemes constituted outside Singapore.

Keep in mind that approval can be on share class level, which is why one fund can have both registration types. Further details are available in the ‘CIS Practitioner Guide’, last updated on 13 March 2020 (also accessible here).

Similar to Switzerland, you can combine the information on the fund’s domicile with the legal registration data (OFST6030SG) and the marketing distribution information (OFST6031SG) to obtain the fund’s registration status and the categories of permitted investors.

Passporting in the European Union according to AIFMD

In Europe, there are non-UCITS funds, which are regulated by the Directive 2011/61/EU on Alternative Investment Fund Managers (AIFMD). These AIF (Alternative Investment Funds) can be distributed in the European Union (EU) by designated AIFM (Alternative Investment Fund Managers).

If the AIF is not marketed in a certain EU country to retail investors, but passported for marketing to professional investors, please indicate this as following:

- ‘Legal Registration’ = ‘res’

- ‘Marketing Distribution’ = ‘res’ or ‘no’

Marketing to retail investors in the EU is primarily a local, jurisdiction-specific process requiring authorization from national regulators, often involving strict prospectus requirements. While the AIFMD passport exists for professional marketing, retail distribution usually relies on national private placement regimes (NPPRs) or specialized structures like ELTIFs. In such cases, the specific countries where permission for retail investors has been obtained should be indicated by ‘Legal Registration’ = ‘yes’.

Other countries

There are further countries such as Australia, the US, Italy, Liechtenstein, Denmark etc., which have different approval types. Please always follow the same pattern:

- Legal approval/registration for all investors: ‘Legal Registration’ = ‘yes’

- Legal approval for restricted audience/certain investors only: ‘Legal Registration’ = ‘res’

- Set ‘Marketing Distribution’ equally to ‘Legal Registration’. If you want to reduce visibility, you can narrow the filtering by choosing the appropriate ‘res’ or ‘no’ value.

For all countries, keep in mind to avoid invalid combinations (such as ‘Legal registration’ = ‘no’/ ’Marketing Distribution’ = ‘yes’).

If a registration approval is pending, please populate ‘no’ until you receive approval confirmation from the local authority.

Special case: Hong Kong Professional Investor (PI) exemption

Foreign funds that are not authorised by the Securities and Futures Commission (SFC) may not be publicly offered in Hong Kong. However, such funds may be offered on a private basis to professional investors as defined in the Securities and Futures Ordinance (SFO), Schedule 1, and the Securities and Futures (Professional Investor) Rules (Cap. 571D).

As these funds are neither SFC-authorised nor publicly marketed in Hong Kong, and information regarding such products may only be made available to a limited category of investors, openfunds recommends reflecting this situation as follows:

- OFST6030HK ‘Legal Registration’ = ‘no’

- OFST6031HK ‘Marketing Distribution’ = ‘no’

Although private placement to professional investors may still be possible under statutory exemptions, this does not constitute marketing in Hong Kong, which is why openfunds currently recommends keeping the Hong Kong Marketing information (OFST6031HK) as ‘no’.

Further information can also be found here:

- https://www.elegislation.gov.hk/hk/cap571D!en.pdf?FROMCAPINDEX=Y

- https://www.sfc.hk/sfc/doc/EN/faqs/products/faq_offers_of_investments_eng.pdf

Document Information

| Title: | Countries of Registration |

| Language: | English |

| Confidentiality: | Public |

| Authors: | openfunds (Michael Partin, Birgit Partin) |

Revision History

| Version | Date | Status | Notice |

| 1.4 | 2026-03-23 | Final | Refresh of layout, update of URL to updated CIS practitioner guide, addition of HK PI example and added further text on L-QIF and SG recognised and recognised restricted scheme. |

| 1.3 | 2024-08-16 | Final | Addition of L-QIF in the Swiss section. |

| 1.2 | 2023-12-15 | Final | Amending Swiss section to reflect change in law regarding non-registered funds. |

| 1.1 | 2022-03-07 | Final | Added versioning details. |

| 1.0 | 2018-11-14 | Final | First version. |

Implementation

If you have any questions about openfunds or difficulties with implementation please contact us at businessoffice@openfunds.org.

Joining openfunds

If your firm has a need to reliably send or receive fund data, you are more than welcome to use the openfunds fields and definitions free-of-charge. Interested parties can contact the openfunds association by sending an email to: businessoffice@openfunds.org

openfunds.org

c/o Balmer-Etienne AG

Bederstrasse 66

CH-8002 Zurich

Email: businessoffice@openfunds.org

If you wish to read or download this white paper as PDF, please click here.